According to a new Fidelity survey with companies offering a defined contribution (DC) plan sponsors with 50-10,000 employees using a variety of record keepers, plan sponsors are focusing more on their plan advisor perhaps due in part to the new DOL conflict of interest rule. So while overall satisfaction with plan advisors has risen 26% since 2011, a high of 23% are actively looking for a new advisor.

According to a new Fidelity survey with companies offering a defined contribution (DC) plan sponsors with 50-10,000 employees using a variety of record keepers, plan sponsors are focusing more on their plan advisor perhaps due in part to the new DOL conflict of interest rule. So while overall satisfaction with plan advisors has risen 26% since 2011, a high of 23% are actively looking for a new advisor.

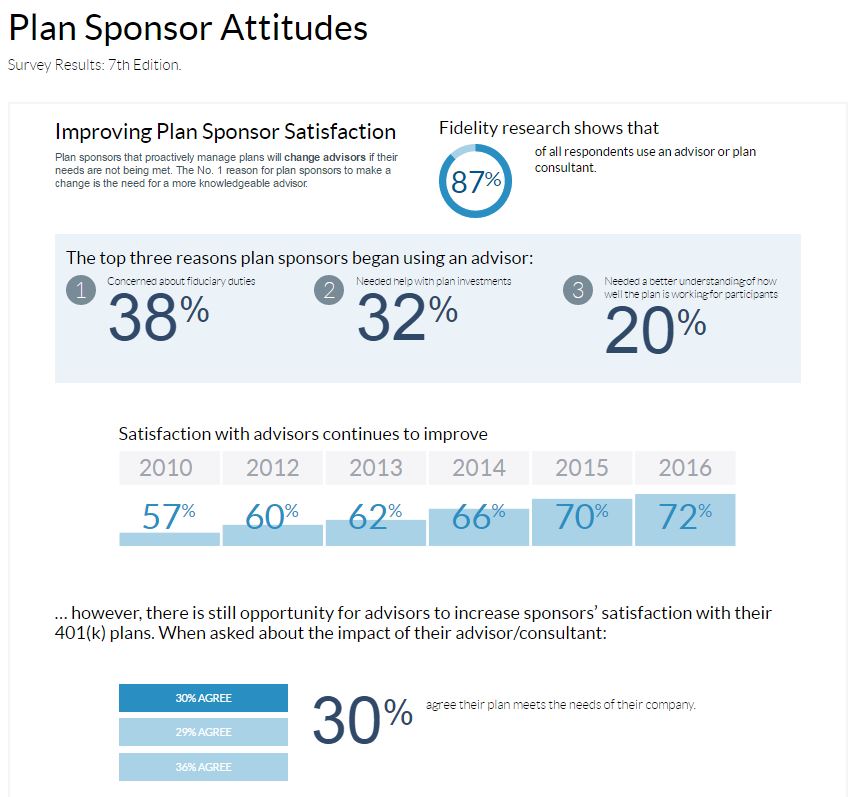

Highlights of Fidelity’s 7th survey with DC plans sponsors about their plan advisor include:

- The number one reason to change advisors is to find a more knowledgeable professional

- Advisors are used to help with:

- Limiting fiduciary liability

- Investments

- Making sure that the plan meets the needs of their employees

With 87% of plans using an advisor or consultant, more DC plans sponsors are realizing that they need to engage an expert to help them manage their plan. The DOL conflict in interest rule, forcing more advisors to act as fiduciary as a result of a broadened definition, seem to be making plan sponsors more discerning about the advisor they choose. Almost 70% of plan sponsors surveyed want their advisor to act as a co-fiduciary.

Ten years ago, massive record keeper consolidation began winnowing the ranks from well over 100 providers to under 40 national record keepers as plan sponsors, with the help of advisors, starting demanding more conducting formal RFPs focused initially on cost cutting but ultimately the quality of the service. The DOL rule is ushering in a similar process for advisors.

Though 250,000 advisors are working or getting paid on a DC plan, just 25,000 are minimally qualified with at least 5 plans and $25 million of DC assets and just 1% or 2500 are Elite Advisors with over $250 million, 10 plans and over 10 years’ experience. The ranks of emerging advisors will be forced out not just because of more sophisticated plan sponsors using a formal advisor RFP process requiring co-fiduciary status but also because broker dealers will not allow many of these dabblers to serve as a DC fiduciary forcing plan sponsors to find an alternative giving rise to “robo-fiduciaries” like Morningstar.

But just because an advisor is willing to act as a co-fiduciary does not make them qualified. Experience, real training from established universities, resources and cultural fit are much more important. Regardless, the focus on fiduciary status by the DOL will force a sea change because, as Warren Buffet once opined, “Only when the tide goes out do you discover who’s been swimming naked.” And make no mistake – the DOL effective April 10, 2017 is a tide turner.