Pew: Retirement Plan Access, Savings Rates Improving Among Younger Workers. Increasing numbers of younger Americans have access to retirement savings plans at work, according to research from the Pew Charitable Trusts. As a result, retirement savings rates are improving among younger workers.

The Pew study analyzed data from the Census Bureau’s Survey of Income and Program Participation (SIPP) on plan access, take-up rates, and overall participation in defined benefit (DB) and defined contribution (DC) plans from 1996 and 2008 for workers ages 18-31. Pew divided workers into two age groups: 18-24 and 25-31, to account for the fact that many younger workers may be finishing school or gaining work experience, both factors that may impact the accuracy of the data. Pew justifies its rationale for tracking the experience of the youngest workers because it believes doing so is helpful to broaden our understanding of the nation’s overall retirement landscape.

Pew defines the metrics used in the study as follows:

“Access represents the percentage of workers who reported that their employer offered a retirement plan. Take-up measures the percentage of workers who reported saving in a workplace retirement plan that was available, while participation captures the percentage of all workers participating in a workplace plan regardless of whether they have access to a plan through their employer.”

Here are some of the key findings from the survey:

- Young workers have higher overall plan balances in defined contribution accounts than the previous generation.

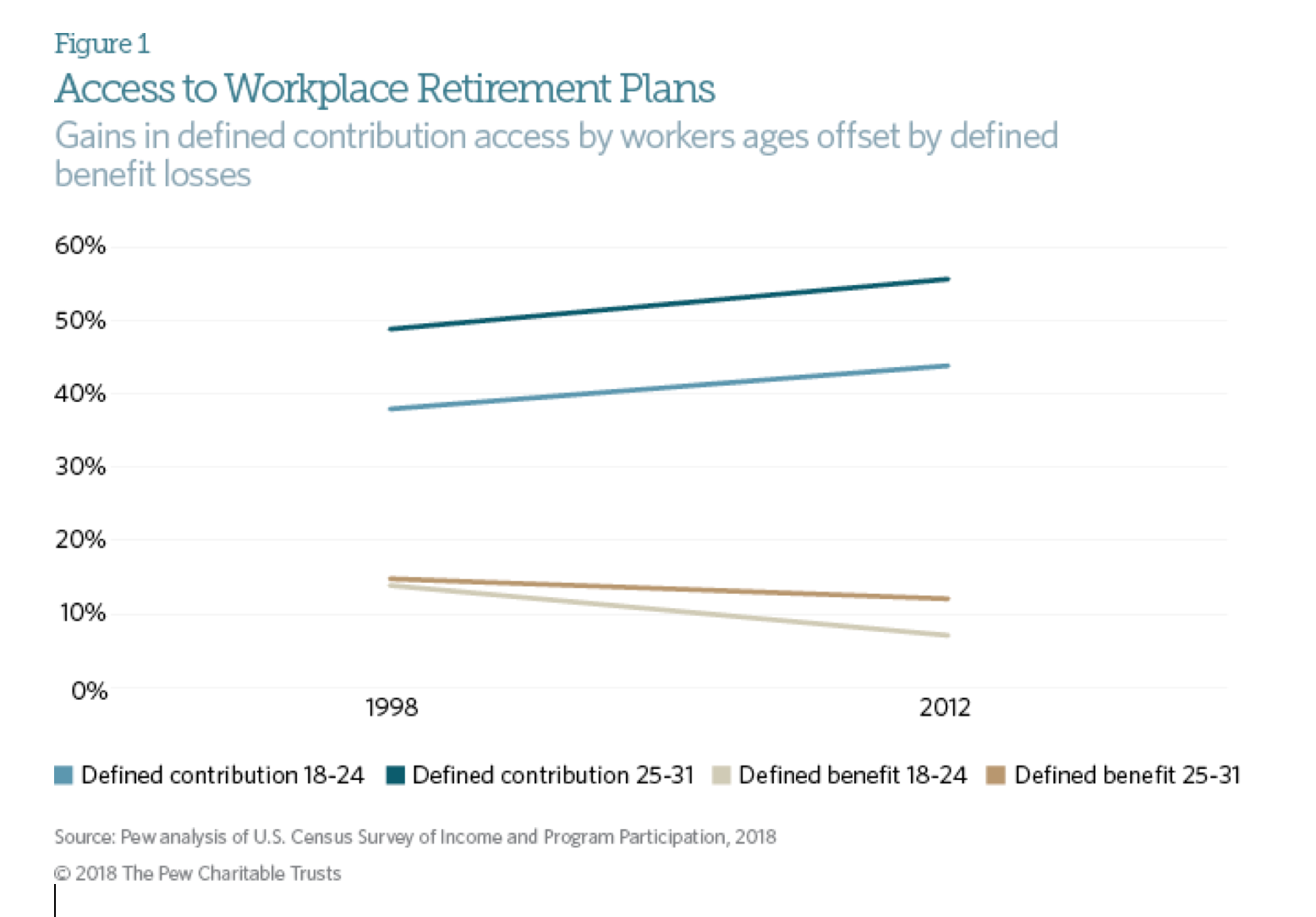

- Gains in access to defined contribution (DC) plans were offset by lower rates of access to defined benefit (DB) plans for workers both ages 18-24 and 25-31. The result is that overall rates of access for young workers remained unchanged between 1998 and 2012.

- Although access overall remained constant, take-up increased in both defined contribution and defined benefit plans for workers ages 25-31.

- Participation increased for workers ages 25-31, largely driven by increases in defined contribution plan participation.

- Men and women had similar rates of access, take-up, and participation.

- Men ages 25-31 saw increases in access and participation while women ages 25-31 saw increases in access and take-up.

- Hispanics lagged substantially behind both blacks and whites of the same age in 2012. However, Hispanics ages 25-31 saw the greatest increases in access of any racial or ethnic group.

- Hispanics ages 25-31 increased their access to retirement plans from 44 percent to 51 percent from 1998 to 2012. Still, two-thirds of blacks and nearly three-fourths (72 percent) of whites had access to plans in 2012.

As the graph below illustrates, a greater number of younger workers gained access to DC plans, while access to DB plans dwindled at similar rates. These findings are not news to anyone who’s been paying attention — DC plans have obviously supplanted DB offerings as the primary workplace retirement savings vehicle. However, they serve as a good reminder that millennials are the first generation to rely solely on DC plans as their primary means of saving for retirement. As such, plan sponsors should pay particular attention to participation rates among this age group, and rely heavily on plan design features like automatic enrollment to help overcome inertia.

That said, Pew found that younger workers ages 18-24 had substantial gains in their plan balances — nearly equal to the average plan balance of older workers. However, workers in that cohort showed limited improvement in their savings’ benchmarks from 1998 to 2012, while workers age 25-31 had noteworthy increases in access, take-up, and participation in workplace retirement plans. According to PEW, this is encouraging, as it seems to signal that workers are catching on that they are primarily responsible for their financial security in retirement.

That said, Pew found that younger workers ages 18-24 had substantial gains in their plan balances — nearly equal to the average plan balance of older workers. However, workers in that cohort showed limited improvement in their savings’ benchmarks from 1998 to 2012, while workers age 25-31 had noteworthy increases in access, take-up, and participation in workplace retirement plans. According to PEW, this is encouraging, as it seems to signal that workers are catching on that they are primarily responsible for their financial security in retirement.

Pew presumes that automatic enrollment is playing a significant role in workplace retirement plan take-up and participation, particularly among the older cohort of workers it studied. Conversely, younger workers may not view retirement savings as a top priority since, for them, it’s an event that’s still far off in the future. As such, they may choose to focus instead on more near-term financial goals such as paying off debt or saving for a house. Logically, the earlier we can encourage workers to participate and start saving in the plan, the more we can help them improve their long-term financial security. As we know, automatic enrollment is an effective tool to help accomplish those goals.