Improving Retirement Plan Outcomes Meets Employees’ Older Selves

Improving retirement plan outcomes may be as simple as getting employees to envision their older selves living the lives, they imagined in their post-work years. Doing so may motivate employees to save more, it turns out. Of course, higher savings rates can make a big impact when it comes to improving retirement plan outcomes.

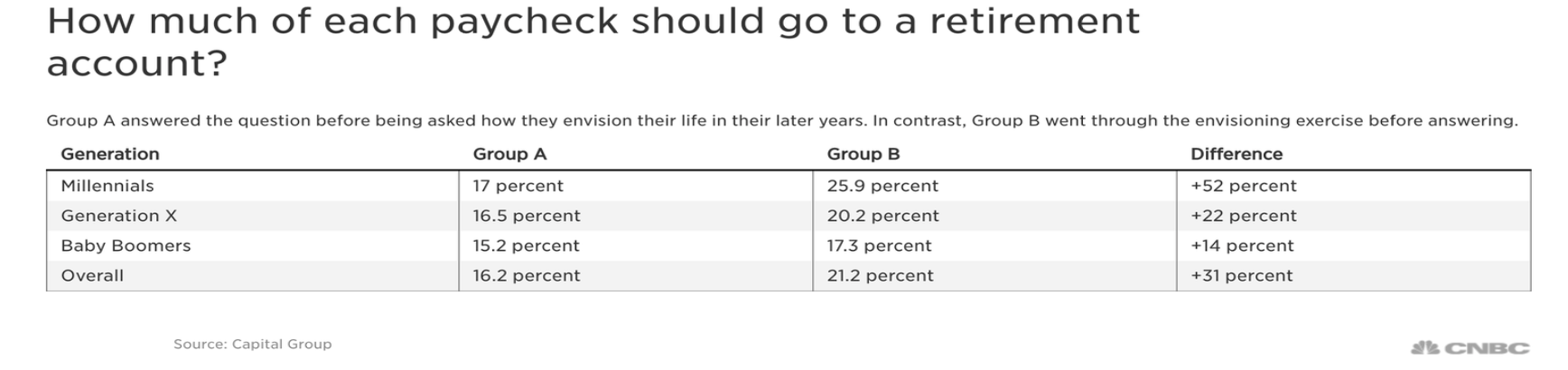

A new survey from Capital Group, cited by CNBC, found that when employees visualized their ideal retirement, they actually recommended saving more for retirement per paycheck than those who didn’t give much thought to their post-career life. The following chart shows the results of Capital Group’s “hidden experiment” in which they asked two groups of people how much of their paycheck they thought they should save for retirement.

One group did the envisioning exercise before answering, and the other did not:

Capital Group surveyed 1,202 adults in April, first asking half how much they should set aside for retirement, then asking them various questions about how they envisioned their lives in their 60s, 70s, and 80s. For the other half, the latter questions came first, then they answered how much they thought they should save. The group that conducted the visualization exercise recommended saving 31% more, on average. The suggested savings were 52% higher on average for Millennials.

As such, visualization exercises like this can be a powerful incentive to prompt employees into improving retirement plan outcomes by increasing their savings rates. And as an industry, we know the importance of boosting retirement plan contributions to achieving the goal of improving retirement plan outcomes. Workers should generally be saving twice what they are, according to data from the Stanford Center on Longevity, also cited by CNBC.

When it comes to improving retirement plan outcomes, employers should consider inventive ways to help employees to imagine and “connect” with their future selves. According to another article from Forbes, people can potentially save more money for retirement by “getting to know” their future selves. Otherwise, we get mired in what social psychologists call “the end of history illusion” — which is the phenomenon of assuming that we will be much the same as we are now in the future, with the same knowledge, preferences, attitudes, point of view, etc. as we have today.

However, it can be difficult for people to imagine themselves as older versions of their current selves. According to Hal Hershfield, Assistant Professor of Marketing at UCLA’s Anderson School of Management (with which The Retirement Advisor University (TRAU) is a collaboration), we see our older selves as strangers, not who we actually are, which is what makes it so challenging for us to envision ourselves getting older. However, this disconnect between our present and future selves can cause us to put off, or even avoid, making critical financial decisions in the present that will be beneficial in the long term, such as saving for retirement. Temporal discounting, people’s tendency to place more value on choices and experiences that give us immediate gratification rather than waiting or investing for a future outcome we have trouble visualizing, also plays a role, according to the Forbes article.

That said, the power of technology can help people connect to their older selves and assist employers in improving retirement plan outcomes. For example, there are apps available that enable us to come face to face with an older version of ourselves by giving us the capability to instantly “age” a current photo. Hershfield used this idea in his research, finding that people who used a tool that included an aged photo of themselves were likely to contribute 6.2%-6.8% of their pay to a workplace retirement plan, compared to just 4.4%-5.2% on average for those who used a tool that included a current photo of themselves.

Now, employers don’t necessarily have to connect employees to smartphone technology to help them save more for retirement, although it certainly would be more fun. Nonetheless, calculators that show the difference a 1%-2% contribution can make, or plan design features such as auto-escalation can prompt employees to save more and help with improving retirement plan outcomes. And visualization exercises clearly have an impact on getting employees to save more. In short, helping employees connect to their older selves, whether it’s accomplished through the power of technology or the mind, can help boost contribution rates, giving employers additional options when it comes to improving retirement plan outcomes.