Navigating the fiduciary requirements and expectations associated with overseeing a tax qualified retirement plan is no easy task. Since many employees are thrust into their newly appointed fiduciary role without fiduciary education or proper training, each quarterly benefits committee meeting can become an exercise in suppressing the look of surprise. As a fiduciary, one quickly understands that the element of surprise is not a coveted emotion.

Navigating the fiduciary requirements and expectations associated with overseeing a tax qualified retirement plan is no easy task. Since many employees are thrust into their newly appointed fiduciary role without fiduciary education or proper training, each quarterly benefits committee meeting can become an exercise in suppressing the look of surprise. As a fiduciary, one quickly understands that the element of surprise is not a coveted emotion.

Fiduciary Surprises come in all Sizes

Upon learning that a company retirement plan has been selected for a Department of Labor audit, a knowledgeable retirement committee fiduciary will likely function at a heightened state of awareness until the audit has concluded. A bigger fear may be the anticipation of being in receipt of a registered letter whereby you and your retirement committee colleagues are named defendants of an ERISA fiduciary breach. Both hypotheticals. What if, workers learn that a group of benefit plans are woefully underfunded and there is no plan to fund or improve the funding status of the plans?

Could you be responsible for the shortfall of thousands of underfunded defined benefit plans and if so, how might that occur?

Expense that Looms on the Horizon

Those who have spent their entire working careers participating in 401(k) plans may be unaware; but there is a Defined Benefit graveyard where under-funded Pension Plans go before they go away forever – the Pension Benefit Guarantee Corporation (PBGC). The PBGC is a federal agency established in 1974 for the purpose of protecting Pension Plan benefits for workers. The U.S. Government is facing a financial-conundrum as the deficit of the PBGC continues to grow. The combined deficit of multiemployer plans and single employer plans currently sits at $79.4 Billion dollars – according to the PBGC 2016 Annual Report (See Page 10 / at the bottom of Table 1).

In the Annual Report, PBGC Director, W. Thomas Reeder states, “We are working to remedy the financial troubles of PBGC’s Multiemployer Program, which is expected to run out of money in the near future.” This, in the Annual Report – where the subtitle reads: ”Keeping Our Commitment to America’s Workers.”

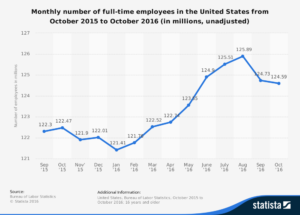

Quick-math on the PBGC Deficit ($79.4 Billion Deficit), divided by the Department of Labor’s October 2016 statistic of full time workers (124.59 million people) leaves an existing unfunded Pension Obligation of $637.29 for every full-time worker. That number alone is not daunting. However, some hard working individuals may see their $637.29 Pension Obligation as menacing or critical – if they cannot pay it. In that case, your portion of your unfunded Pension Liability may double or quadruple or increase by an even larger factor.

Individuals who assume their only future-funding obligation is their own 401(k) may be surprised at the time our nation’s growing PBGC Deficit is apportioned to all full-time workers. At that point, the number becomes ominous.