Target Date Funds (TDF) continue to dominate retirement asset growth.

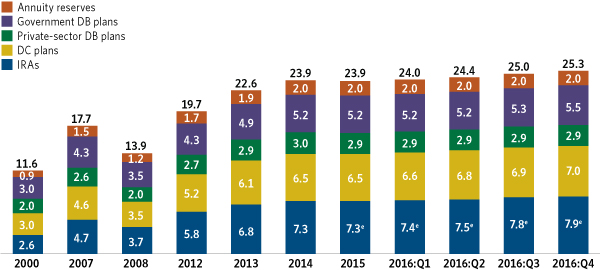

Now accounting for over one-third of household assets, US retirement assets led by IRAs and defined contribution (DC) plans grew to $25.3 trillion up from $23.9 trillion in 2015 a burst of 6.1% according to ICI*. IRAs and DC plans led the way accounting for $14.9 trillion or almost 60% of the totals while DB plans remained stagnate at $2.9 trillion or just 11%.

Of DC assets, 401k plans included $4.8 trillion or 63% followed by 403b plans, the Thrift Savings Plan and 457 plans. 401k plans grew a stunning 8.5% in 2016 led by the growth of target date funds (TDFs) which have increased to $887 billion, a 16.3% increase. Mutual funds still dominate 401k plans with a market share of 63% or $3 trillion led by equities at $1.8 trillion or 37.5%; TDFs are catching up accounting for 12.7% with $835 billion in 401k plans.

The ICI report highlights a few obvious shifts in the investing and retirement world:

- Retirement is becoming more important to investors, plan sponsors and the financial services industry AT $25.3 trillion and one-third of household assets.

- Money in DB or pension plans is decreasing taking away market gains with more emphasis on DC, especially 401k plans.

- IRAs are the focus of the DOL conflict of interest rule for good reason – that’s where the money is fueled by rollovers from DC plans.

- The growth of TDF continues due to their dominance as the default option (QDIA) attracting a large percentage of new contribution.

Other trends are the move to CITs not just in the large market but for smaller plans led by larger advisor groups pooling assets of clients as well as the growth of index or passive investing. Government entities struggling with an estimated $4 trillion DB deficit are moving to DC-like plans which will continue.

But it only gets harder from here as investors struggle to save enough for retirement and companies, trying to stay competitive, are burdened with higher costs of older workers not able to retire. Active money managers without a TDF strategy fight over fewer assets and the shift to lower cost index funds has significantly affected their bottom line. The fight over participant data between advisors and record keepers is just starting as both parties look to mine relationships with over 80 million people.

*Sources: Investment Company Institute, Federal Reserve Board, Department of Labor, National Association of Government Defined Contribution Administrators, American Council of Life Insurers, and Internal Revenue Service Statistics of Income Division