Limited Investment Menu Choices Better for Participants?

In a recent report by American Funds on Defined Contribution (DC) investment choices…the choice is clear; less is more. Confused? Well, that was the point. The DC plan white paper by American funds looked at the issue of whether more investment choices in a plan menu was beneficial versus fewer investment choices. The results of the study suggest that fewer options in the investment menu resulted in better outcomes.

Defined benefit (DB) plans consistently report better returns — as much as 0.9% higher per year1 — than defined contribution (DC) plans. The Pension Protection Act gave plan sponsors tools to narrow this gap, such as investment re-enrollment and target date funds (TDFs) as default investments. These have helped improve investing behavior for many participants, but what about the 63% of DC plan participants who still make their own investment decisions?2 Plan sponsors can set up better decision-making from these participants by simplifying their investment options. Fewer and easier-to-understand menu choices can encourage more appropriate selections, leading to better potential outcomes. Sponsors can facilitate this with a few steps:

-

Reduce the number of menu options to simplify decision-making.

-

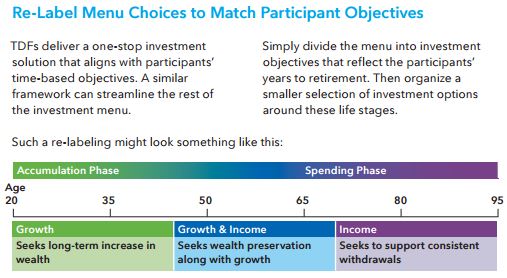

Re-label menu options around easily understood life goals to better align with participants’ retirement objectives.

-

Re-organize menus using broader more flexible options to maintain diversification with fewer choices.

–Defined Contribution Investment Perspectives

The Evolution of Investment Menu Design

In “Simplify Menus to Meet Participant Objectives,” American Funds Vice Presidents Toni Brown, John Doyle, Craig Duglin and Sue Walton argue that offering many investment choices discourages engagement (causes stress and confusion) in a retirement plan versus few choices which result in better outcomes and higher engagements. “Complex menus lead to participant confusion, disengagement and poor investment decisions,” says the study.

The authors: Brown, Doyle, Duglin and Walton outline three steps by which they contend plans can facilitate better choices.

Offer fewer menu options.

Brown, Doyle, Duglin and Walton cite research backing the notion that people in general respond better when offered a smaller array of choices than a large one, including retirement plan investment options. In fact, they posit that a large number of choices can be debilitating. “It’s not uncommon to see this paralysis in decision-making take the form of counterproductive investing behaviors like 25-year-olds investing 100% into money market funds and 65-year-olds not adjusting their 100% equity positions,” they say.

Re-label menu options.

The paper argues that another way to facilitate greater engagement and better choices by plan participants is to label menu choices so they better match participants’ objectives and goals. This can be accomplished, they suggest, by grouping investment choices into categories that correspond to participants’ ages. “Such an approach makes it easier for participants to see how their investments relate to their life stage,” it says. As such, “they may be more likely to make decisions that support investment success.”

Offer broader, more flexible options.

Brown, Doyle, Duglin and Walton suggest that merging investment choices into broader categories can simultaneously reduce the number of options and make the menu of choices more flexible, while still covering the same spectrum. “Participants may better resonate with their choices if the new menu options are re-labeled using the objective-based framework of ‘growth’ and ‘income’ rather than ‘equity’ and ‘fixed income,’” they write.